What to Expect When You're Expecting (To Raise Capital)

Are we in a bubble? How much dilution is too much dilution? A look at the state of early stage funding in Israel

To put it lightly, 2020 has been a tumultuous year. And as it comes to a close, it’s been fascinating to reflect on the shifting sands of the Israeli early stage venture market. From being a relatively quiet market at the initial stages of the pandemic, to becoming the most competitive period of time I have witnessed in my years as a VC, it’s truly been a whirlwind of a year.

Due to the up and down nature of the market though, some fundamental changes have occurred relating to early stage funding. The following are some of my observations.

Seed Rounds in 2020

Seed rounds in 2020 have undergone a metamorphic shift. Gone are the days of the $1m-$2m seed round. The average seed round in today’s market sits anywhere between $3m-$6m for first time founders, and well over that for serial entrepreneurs. But what should entrepreneurs expect from a dilution perspective when raising these rounds? Well, there are a few things that need to be considered:

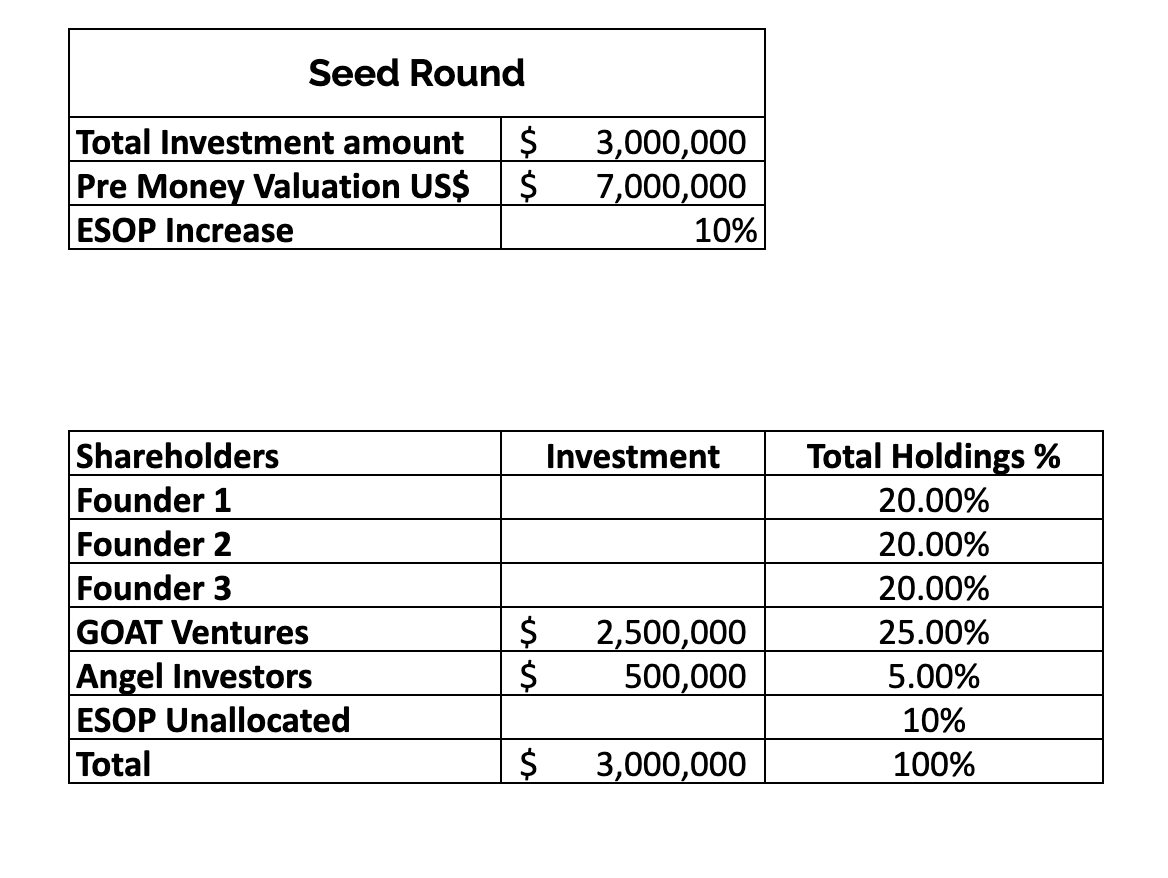

The number one thing that founders should understand is that a seed round valuation is a derivative of VC ownership targets. Let me explain: if GOAT Ventures targets 25% ownership, and you are raising $3m, that would imply a $12m post-money valuation. 3/25% = 12. It’s as simple as that. Sort of.

The second thing that founders need to keep in mind is the employee stock options pool (ESOP). This option pool is defined during your round, and will serve as the bank of shares that you can offer early employees who join your company. The standard size of ESOP is 10% for seed rounds, and 5% for A rounds. Experienced founders and/or competitive deals can drive the ESOP size a few percentage points lower, but it’s important to note that this dilution usually affects only pre-existing members of the cap table. In other words, GOAT Ventures wants to hold 25% of the company, AFTER the ESOP has been issued. So in addition to the 25% dilution from your VC, tack on an additional 10% for ESOP, which takes us to 35% total dilution.

The third thing that founders should think about is the number of investors investing in the round. While GOAT Ventures is leading the round, perhaps they are only willing to commit around 85% of the capital you are looking to raise ($2.5m out of a total $3m in our example)*. They still, however, are targeting 25% ownership. So now your implied valuation is actually $10m post money valuation, and let’s tack on an additional 5% dilution for the remaining $500k that you need to raise (0.5/10 = 5%). Now your total round’s dilution sits at 40%.

*As an aside, GOAT Ventures may be willing to invest the full $3m, but you might want to add additional angel investors to the round. This is where getting creative comes in handy.

Benchmarks

For seed rounds of $3m-$6m, anywhere between 25%-40% total dilution should be expected

Competition drives valuation up, which drives dilution down

If you want to raise from multiple VCs, expect the total dilution to be closer to 40%, or even exceed it. As mentioned, GOAT Ventures has their ownership target, and Mamba Ventures has a similar ownership target as well

ESOP size should be around 10%

I’ve seen anywhere from 8%-12% at the seed stage

Solo founders should expect VCs to request closer to 15%, but it’s very situation dependent

For A rounds, total expected dilution should be anywhere between 20%-30%, and ESOP size should be between 5%-7%

ESOP size at the A round is largely dependent on how many of the senior management roles have already been filled

Capital raised should be budgeted to last for 18-24 months. As I’ve written in the past, there’s no need to reach a specific revenue benchmark or other arbitrary KPI prior to raising your next round. Rather, focus on creating positive momentum around the company about 8-10 months prior to end of cash date

Blowing Bubbles

Round sizes have gotten larger, valuations have increased, time to term sheet has decreased and the concept of having actual business progress prior to raising a round has become largely unnecessary. Is this evidence of a bubble? Perhaps. But I’m not a macroeconomic expert. What I can tell you is that despite what some people may have you believe, there has never been a better time to raise capital. This has been caused by a few factors.

First and foremost, there has been an influx of international late stage capital at the early stages. Firms like Insight and Accel are investing quite actively at the seed and A stages, not to mention their continued activity in traditional later stage rounds. This has put pressure on local later stage funds to invest in earlier stage companies as well. So if traditional B round and C round investors are now investing in A rounds, traditional A round investors have no choice but to follow suit and move downstream themselves and focus their efforts on seed rounds. And just as their late stage counterparts, one of the best tools in their sheds to win deals over traditional seed investors is their ability to offer more capital for similar dilution. This has led to the virtual disappearance of the traditional $1m-$3m seed round, and with it the demise of local micro funds.

Secondly, many funds spent Q1 and the early part of Q2 on the sidelines in order to see how the market would react to the pandemic. Once they observed that tech companies were relatively unaffected, they reentered the market aggressively with “extra” capital to deploy in order to make up for lost time. This and the previous factor have brewed a perfect storm for a very competitive early stage financing climate.

Anecdotally, I have never seen the market as active as it’s been in the past six months. But interestingly, I also do not recall meeting such a high volume of truly exceptional founders in a such a short time frame. It’s possible that the sheer quality of founders in the market today, which is a result of a continuously maturing local ecosystem, has also led to a natural increase in valuation and round size.

Although I mentioned that the average seed round today sits between $3m-$6m, it may be tempting for founders to raise a much larger $6m-$10m seed round, as the capital is available. To founders considering this, I’d like to offer a few words of caution.

No capital is free. See the previous two sections of this post and understand that raising a large seed round will likely have very significant dilution ramifications for your company

For a seed round size this large, you will most likely need to have two VCs involved.

While it may seem counterintuitive, having too much capital early on can negatively effect hiring. With so much money in the bank, you may begin to allow yourself to hire the best, and second best candidate that you interview for a position. But this can be detrimental to your company’s success as you are de facto lowering the bar for working at your company. It’s nearly impossible to resist the temptation to hire two great people - having less money in the bank will help make the decision for you

As Always, Context is Key

Context is always the most important caveat, especially when raising a round of financing. Optimizing for a percentage point here or there probably isn’t the smartest way to go about fundraising and as I’ve written in the past, you should be optimizing for the person/firm you will be working with. Lastly, the benchmarks I mentioned are based on what I’ve seen over the past 6-12 months, they could change very quickly. So it’s always best to ask your fellow founder friends for advice.