Let's Talk About Value Add

Let's Talk About Value Add

Funds like to talk about how much value they bring to the table, but what actually moves the needle?

If you’ve ever met a VC, I’m sure they were quick to tell you about their “value add” - that is, the value that they add to their portfolio companies. In fact, value add has become so synonymous with “smart money” that founders will often ask investors what their value add is if a detailed description hasn’t already been volunteered by said investor.

Today, when people speak about VC value add, they often talk about a firm’s network of potential customers, or lack-thereof. (If you’re raising money in Israel, you wouldn’t be blamed for thinking that every CISO in the world is on an advisory board of one Israeli fund or another). They discuss a firm’s on staff recruiting team that can help founders hire the best talent, and they flaunt their well connected LPs who can facilitate high valued introductions down the road. These efforts are all well and good. Of course, I would never suggest that thinking of ways to help portfolio companies is a bad thing. I simply do not believe that any of the above are legitimate reasons by which to choose your investor.

It occurred to me that not enough people realize, founders and investors alike, that value add is 100% subjective - each company has different needs. Value add is not and should not be considered an all encompassing term that refers to smart money, because depending on the situation the same fund could be considered both dumb money and smart money.

But while it’s easy for me to ponder the deeper meaning of value add, I thought it best to ask our founders what they are looking for from us, both to better serve them and future founders, as well as to crystallize my own thoughts about what value investors can actually provide to truly move the needle.

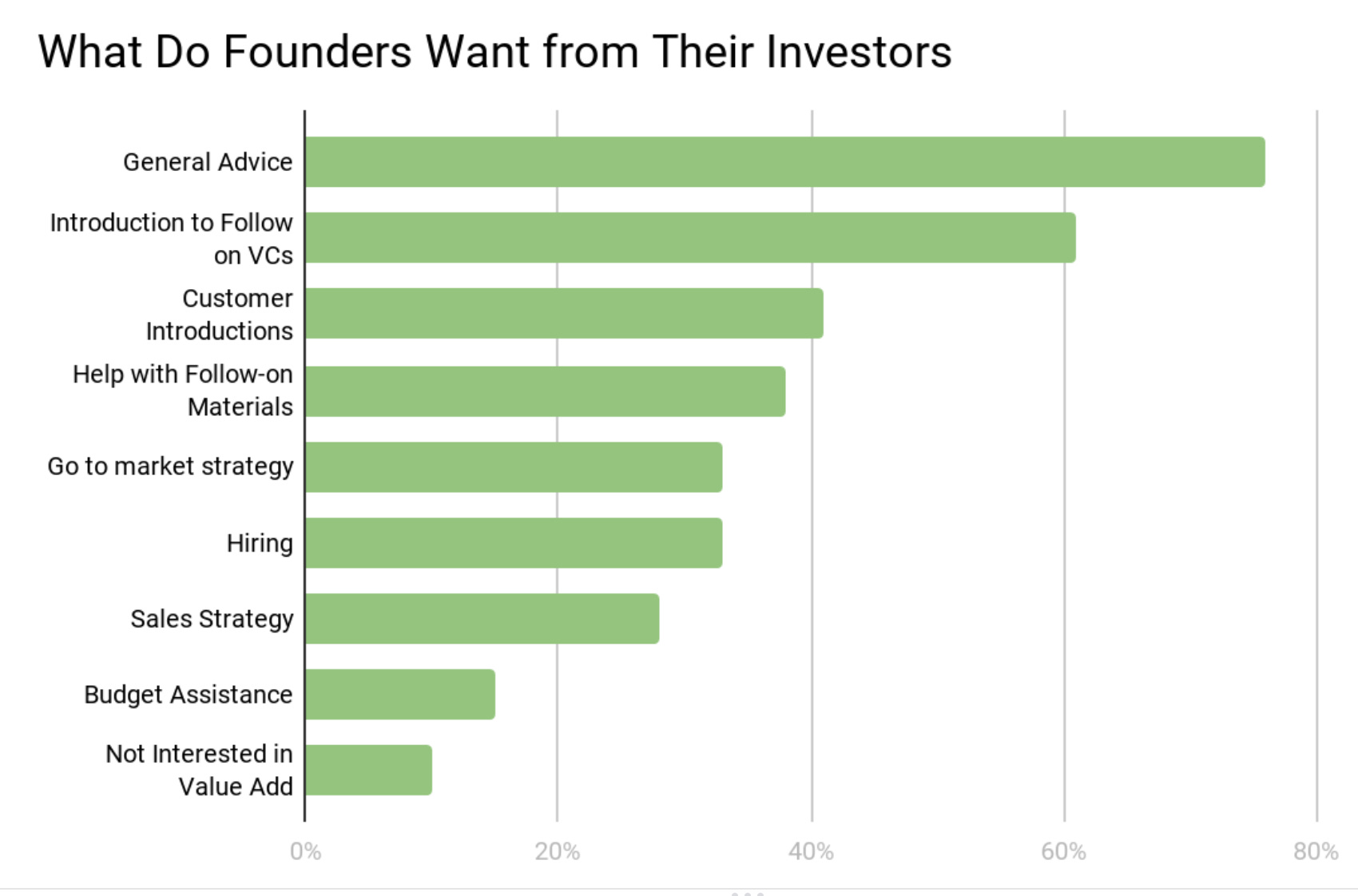

67 founders from the TLV Partners portfolio were polled on what I believe to be the main buckets of “value add”, and you can see the results above. (Please note that founders were allowed to choose as many of the nine options as they wished.)

Takeaways:

“General Advice” was the clear winner. I don’t believe this would have been predicted to garner the most votes by the majority of people out there, but I think it makes perfect sense. Investor value shouldn’t be measured by industry expertise or the number of CISO’s on speed dial, but rather by the personal chemistry established between a founding team and a fund. When choosing an investor, you should over index for approachability, the ability to ask the right questions and the skill of applying lessons learned elsewhere to seemingly unrelated circumstances. To borrow an overused analogy: choosing a VC is like choosing a spouse - you shouldn’t choose your VC based on looks. Make sure you love your VC for what’s on the inside.

Introduction to follow on VCs comes in at #2: As the saying goes - the #1 reason for startup failure is running out of cash. A value add VC should not only be in a position to continue to support you financially in subsequent rounds, but should be in a position to facilitate high level introductions to Tier-1 investors for your next round/s. While you could simply ask each fund that you’re speaking to who their contacts are, VC is a small ecosystem and most funds have “acquaintances” at any future fund you may want an introduction to. But in order to determine a fund’s ability to truly set you up with future cash injections, look at their existing portfolio. Which firms have led follow on rounds in their companies? These are the funds that they likely have the best relationships with.

Customer Introductions: This is the only area where I disagree with our founders. I wouldn’t want to invest in a team that has to rely on their investors for customer introductions. Can your VC help with a few early introductions to design partners? Sure, and 90% of VCs out there will easily be able to help with this. But as a company, you need to be capable of building out a scalable go to market strategy on your own. And VC customer introductions is not a model that scales. Too often, VCs put their ostensibly strong customer connections front and center during a diligence process in an effort to woo founders. Don’t fall for this tactic, it’s not that important.

Hiring: Placing sixth out of nine options, help with hiring placed significantly lower than I would have predicted. I don’t have anything smart to say about this but I wonder if this is simply because founders have given up hope that their investors can effectively help with this.

Aside from being interesting, I hope that this post helps influence at least some founders’ perspectives on the concept of value add. At the end of the day, I know of very few instances where a VC has led to the success of a company, but I know of numerous examples where a VC has led to the failure of a company. Oftentimes founders over index for what they perceive to be value add, when they really should be focusing on founder-investor chemistry.

So the next time you find yourself sitting with an investor, don’t worry about their industry connections or lack-thereof. Rather, ask yourself if the person sitting across from you is someone you want to spend 10 years of your life with. And if the answer is yes, everything else will fall into place.

Good article! (again :) )

Just adding my 2 cents

I think that in hiring, the VC can do a good job helping with that, but most of the time, the founder network or using an employment agency will do the job.

Of course, founders would also like to get help with this :)

As for the customer introduction, it's harder to get the first client to use your product. If the founder can get help from "in-house", that can reduce the time to MVP and from there to success.

Thanks for sharing your thoughts

Interesting. Thanks for sharing